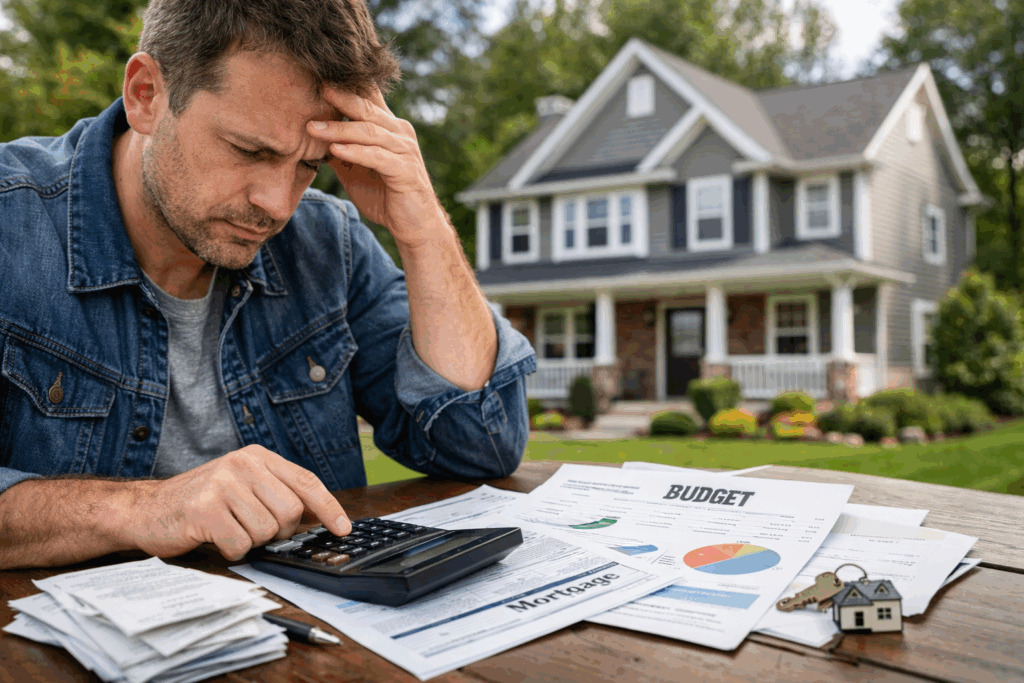

Budget stress is becoming common for buyers in North Jersey as many now spend over 40 percent of their income on housing.

For decades, homebuyers across the country have been told to follow a simple affordability guideline known as the 30 percent rule. The idea is straightforward: spend no more than 30 percent of your gross household income on housing costs, including the mortgage, property taxes, insurance, and association fees if applicable. The rule was rooted in 1969 public housing regulations that originally capped rent at 25 percent of income, later rising to 30 percent in the 1980s.

That number helped generations of buyers avoid becoming house poor. It created a simple benchmark for lenders, agents, and financial planners. In 2025, however, the 30 percent rule has become less of a guide and more of a historical artifact. New data shows that buyers today, especially in high cost states like New Jersey, are routinely spending far above that benchmark.

Recent reporting points to a striking national shift. Buyers are now devoting roughly 43 percent of their income to housing. In markets like North Jersey, where prices rise faster than wages, that number can climb even higher. For many households, the math behind affordability has fundamentally changed.

Why the 30 Percent Rule No Longer Works in New Jersey

New Jersey has always been an expensive place to own a home. Property taxes are among the highest in the country. Insurance premiums have climbed. Inventory remains tight. Wages have not kept pace with home values, and interest rates rose sharply from the record lows of 2020 and 2021.

This created a perfect storm. Buyers who want to remain in New Jersey are being forced to stretch beyond traditional guidelines simply to compete.

Here is why the old rule is breaking down.

1. Home prices have risen faster than incomes

Across Bergen, Passaic, Essex, Morris, and Union counties, median sale prices have increased significantly over the last five years. Even modest starter homes often require buyers to break the 30 percent rule just to enter the market.

2. Interest rates have shifted affordability

Many buyers believed they could refinance later, yet rate relief has been slow. A higher monthly payment is now the norm rather than a temporary inconvenience.

3. Property taxes and insurance are major cost drivers

Even if mortgage rates stabilize, annual carrying costs in New Jersey continue to climb. They are unavoidable, and they push household budgets well beyond that 30 percent threshold.

4. Lifestyle and location needs have changed

Remote work, school preferences, multi generational living, and commute considerations mean buyers are prioritizing convenience and quality over strict budgeting guidelines.

What Spending 43 Percent Really Means for Buyers

Spending over 40 percent of income on housing does not automatically equal financial trouble. Households with strong emergency savings, low consumer debt, or stable job security may manage higher ratios without strain.

However, it does increase vulnerability to economic shocks. In New Jersey, rising taxes, surprise assessments, higher utilities, and HOA increases can quickly tighten a family’s financial outlook. In a competitive market, many buyers accept these risks because the alternative is continuing to rent or being outbid repeatedly.

Buyers also understand that homeownership in New Jersey has offered long term equity growth. Even with high upfront costs, many believe the long play still makes sense.

What New Jersey Sellers Should Take From This Trend

If buyers are stretching further than ever before, sellers benefit. Sellers in North Jersey should pay close attention to these affordability shifts because they directly impact pricing power and days on market.

Here is what this means for you if you plan to sell in 2026.

1. Serious buyers are still active

Buyers are not retreating. They are adjusting. Households who want to stay in Bergen, Essex, Morris, and surrounding counties will stretch their budgets to secure the right home.

2. Overpricing is still risky

Even motivated buyers have limits. Homes with location challenges, deferred maintenance, flood zone issues, or busy road frontage will be judged more harshly. These properties sit unless priced correctly on day one.

3. Updated and well presented homes still command top dollar

Move in ready homes reduce buyer stress. With so much of their income going toward the monthly payment, buyers prefer properties that will not require immediate out of pocket repairs.

4. Distressed homeowners now face more competition

As affordability tightens, an uptick in preforeclosures is expected due to rising taxes, insurance increases, and cost of living pressures. This adds more inventory to the market, which means traditional sellers must position their homes correctly to stand out.

Should Buyers Still Follow the Old Rule in New Jersey?

The 30 percent rule remains a helpful benchmark but not a universal standard. Today’s buyers must consider a more detailed approach.

A modern affordability assessment in New Jersey should include the following:

• Full monthly payment, including taxes and insurance

• Utility costs for an older or less efficient home

• Expected maintenance for aging North Jersey housing stock

• Parking fees or HOA charges in condo and townhouse communities

• Flood insurance requirements in specific neighborhoods

• Long term resale potential based on location and condition

Buyers who ignore these factors often feel financial strain after closing. Buyers who understand them make stronger, safer decisions.

This is where an experienced local agent becomes essential. North Jersey’s affordability puzzle requires precision, local knowledge, and planning, not just broad rules from decades ago.

The Bottom Line: New Jersey Needs a New Affordability Framework

The 30 percent rule was a product of a very different housing market. In 2026, the reality is more complex. New Jersey buyers are stretching further. New Jersey sellers are benefiting from that urgency. However, both sides need guidance grounded in today’s conditions rather than outdated formulas.

If you are thinking about buying, selling, or navigating a preforeclosure or inherited property in North Jersey, I can help you understand your true numbers and your best options.

NJ House Partners combines traditional market expertise with a streamlined hybrid agent approach that gives sellers flexible solutions and real time local data.

You deserve clarity, strategy, and a plan that fits this new marketplace.